Introduction

The escalating confrontation between Iran and the United States has again brought the Strait of Hormuz into the centre of global attention. This narrow waterway is one of the most strategically important locations in the world for energy transport. Any disruption to this route immediately sends shockwaves through the global economy.

Recent military tensions and attacks on shipping near the strait have already caused oil prices to surge and raised fears that a prolonged conflict could destabilise global markets, increase inflation, and push energy costs higher across Europe, including the United Kingdom.

1. What is the Strait of Hormuz?

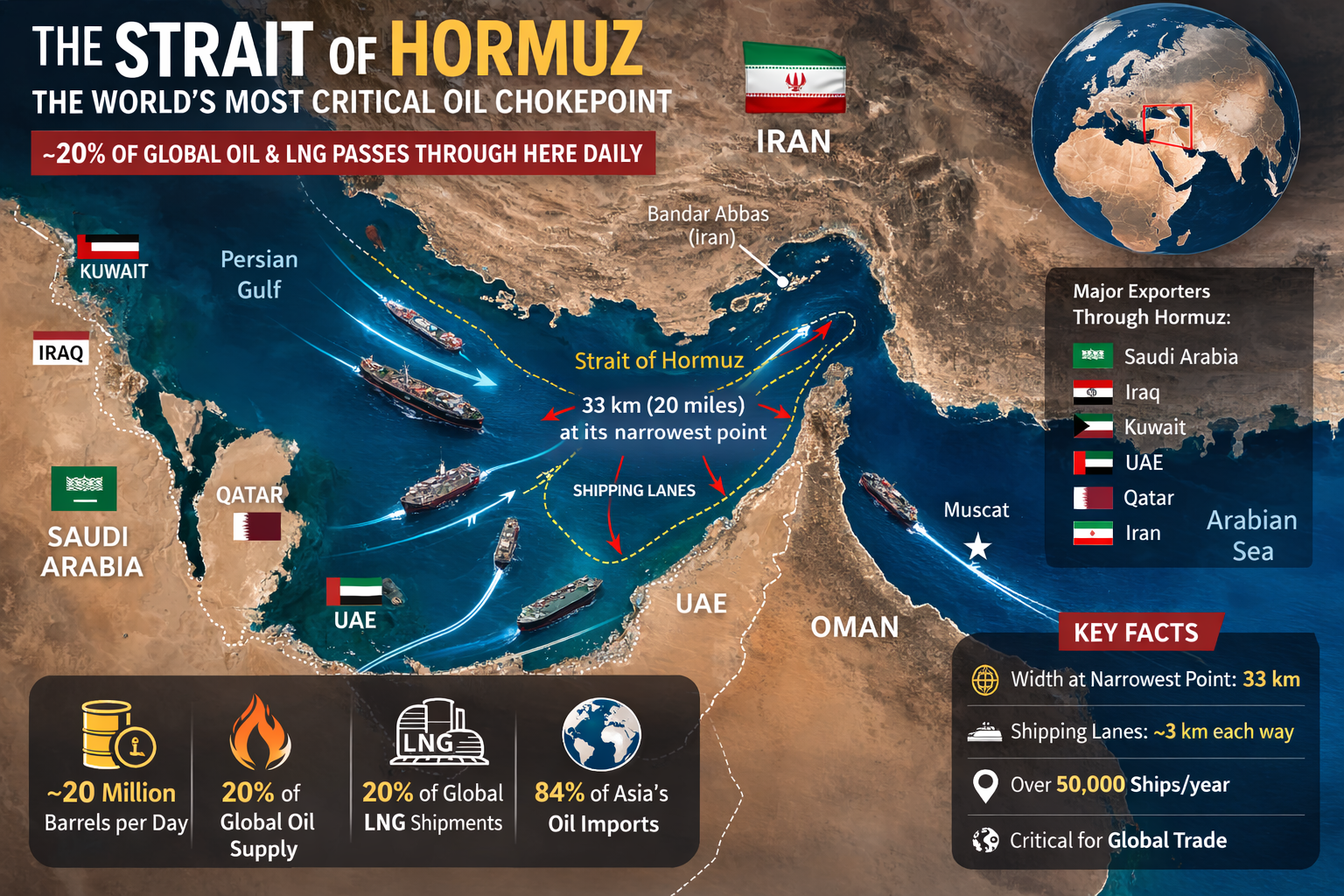

The Strait of Hormuz lies between Iran and Oman and connects the Persian Gulf with the Arabian Sea. It is one of the most critical maritime “choke points” in the world.

Key facts:

- The strait is about 33 km (20 miles) wide at its narrowest point.

- Shipping lanes are only 3 km wide in each direction.

- About 20 million barrels of oil per day pass through the strait.

- This represents roughly 20% of global oil supply and around 20% of LNG shipments.

Major oil exporters relying on this route include:

- Saudi Arabia

- Iraq

- Kuwait

- United Arab Emirates

- Qatar

- Iran

Much of this oil is transported to Asia, which receives around 84% of crude shipments through the strait.

2. Historical Background of Hormuz Tensions

The Strait of Hormuz has been a flashpoint for decades.

Iran–Iraq War (1980–1988)

During the “Tanker War” phase of the Iran–Iraq conflict, both sides attacked oil tankers in the Gulf. The United States intervened to protect shipping lanes.

2000s Nuclear Crisis

Iran repeatedly threatened to close the strait in response to Western sanctions over its nuclear programme.

2019 Tanker Attacks

Several oil tankers were attacked near the strait, escalating tensions between Iran, the US, and Gulf states.

Recent Escalation (2026)

Recent strikes and retaliatory actions have slowed or disrupted shipping traffic and increased fears that Iran could block the passage entirely.

3. Why Closing the Strait Would Shake the World

The global oil system is extremely sensitive to supply disruptions.

If the Strait of Hormuz were closed:

- Up to 20% of global oil supply could be disrupted.

- Global shipping routes would be severely affected.

- Oil tankers might be forced to stop or reroute.

Some analysts suggest:

- Oil prices could quickly rise to $90–$100 per barrel in the short term.

- A prolonged blockade could push prices to $130 per barrel or higher.

Such a price spike would affect transport, food supply, manufacturing, and global inflation.

4. Impact on the United Kingdom

Although the UK does not import most of its oil directly from the Persian Gulf, global oil prices affect everyone because oil is traded on international markets.

Petrol Prices

UK petrol prices usually follow crude oil prices with a delay of about 1–3 weeks.

If the conflict continues:

- Petrol and diesel prices could rise significantly.

- Transport costs for businesses would increase.

- Food and goods could become more expensive.

Energy Bills

Europe relies heavily on LNG shipments from Qatar, which also pass through the Strait of Hormuz.

A disruption could:

- Push European gas prices sharply higher.

- Increase UK household energy bills.

Some analysts warn energy bills could surge dramatically if LNG supplies are restricted.

5. Global Economic Consequences

A long-term closure would affect the entire global economy.

Possible consequences:

- Higher inflation worldwide

- Stock market volatility

- Higher shipping and insurance costs

- Supply chain disruption

Economists warn that a severe oil shock could reduce global economic growth and trigger recession risks.

Even a moderate disruption can push up energy and transport costs across industries.

6. Could Iran Really Close the Strait?

Iran has the military capability to disrupt shipping through:

- Naval mines

- Missiles

- Fast attack boats

- Drone attacks

However, closing the strait permanently would also harm Iran itself.

Iran exports much of its oil through the same waterway, especially to China. A blockade could damage its own economy and anger neighbouring Gulf states.

Military analysts also believe the US Navy and allied forces would intervene quickly to reopen the route.

7. What Is the Likely End Game?

Most experts believe a long-term closure of the Strait of Hormuz is unlikely.

Reasons include:

- Global economic pressure on all sides

- Dependence of Gulf countries on the shipping route

- Potential military intervention by the United States and allies

- Diplomatic pressure from major powers such as China and the EU

More likely scenarios include:

- Short-term disruptions

- Temporary attacks on shipping

- Negotiated de-escalation

Oil markets often spike during crises but stabilise once the immediate risk fades.

Conclusion

The Strait of Hormuz remains one of the most critical strategic chokepoints in the global economy. Any military conflict involving Iran and the United States inevitably raises fears of oil supply disruption.

While a complete and prolonged closure of the strait would trigger a severe global energy crisis, most analysts believe such an outcome would be short-lived due to international pressure and military intervention.

However, even temporary disruptions can drive up oil prices, increase energy costs, and contribute to inflation worldwide. For the United Kingdom, the main impact would be higher petrol prices, increased energy bills, and broader economic pressure.

The ultimate outcome of the current tensions will likely depend on diplomacy, global political pressure, and whether regional powers can prevent a wider war in the Middle East.